Guide to Investing

spin-free guide to investing Investing | Risk | Equities | Bonds | Property | Income

Contents Introduction to spin-free guides 3 Where could you invest? 4 Where you can invest: Bonds 5 Where you can invest: Property 6 Where you can invest: Equities 7 Understanding risk 8 Where you can invest: Multi-asset 9 Some of the ways you can invest 10 Glossary 11 Please refer to the glossary found on page 11 for an explanation of the words highlighted in bold throughout this guide.

guides This brochure is part of our range Spin-free guides aim to give you the basics of spin-free guides: about investing, to help you make informed decisions about your financial goals and how Investing to reach them. Equities The value of investments, and the income from them, will fluctuate which will cause the fund price to fall as well as rise and you may not get back the original amount you invested. We are unable to give financial advice. Risk Income If you are unsure about the suitability of your investment, speak to a financial adviser. The views expressed in this document should not be taken as a recommendation, advice or forecast. Bonds Property 3

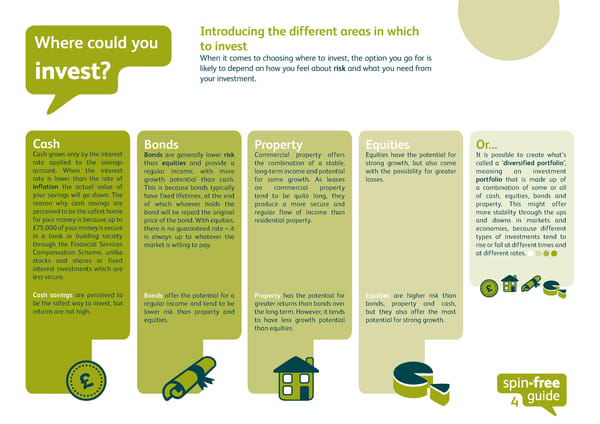

Where could you Introducing the different areas in which to invest When it comes to choosing where to invest, the option you go for is invest? likely to depend on how you feel about risk and what you need from your investment. Cash Bonds Property Equities Or... Cash grows only by the interest Bonds are generally lower risk Commercial property offers Equities have the potential for It is possible to create what’s rate applied to the savings than equities and provide a the combination of a stable, strong growth, but also come called a ‘diversified portfolio’, account. When the interest regular income, with more long-term income and potential with the possibility for greater meaning an investment rate is lower than the rate of growth potential than cash. for some growth. As leases losses. portfolio that is made up of inflation the actual value of This is because bonds typically on commercial property a combination of some or all your savings will go down. The have fixed lifetimes, at the end tend to be quite long, they of cash, equities, bonds and reason why cash savings are of which whoever holds the produce a more secure and property. This might offer perceived to be the safest home bond will be repaid the original regular flow of income than more stability through the ups for your money is because up to price of the bond. With equities, residential property. and downs in markets and £75,000 of your money is secure there is no guaranteed rate – it economies, because different in a bank or building society is always up to whatever the types of investments tend to through the Financial Services market is willing to pay. rise or fall at different times and Compensation Scheme, unlike at different rates. stocks and shares or fixed interest investments which are less secure. Cash savings are perceived to Bonds offer the potential for a Property has the potential for Equities are higher risk than be the safest way to invest, but regular income and tend to be greater returns than bonds over bonds, property and cash, returns are not high. lower risk than property and the long term. However, it tends but they also offer the most equities. to have less growth potential potential for strong growth. than equities. 4

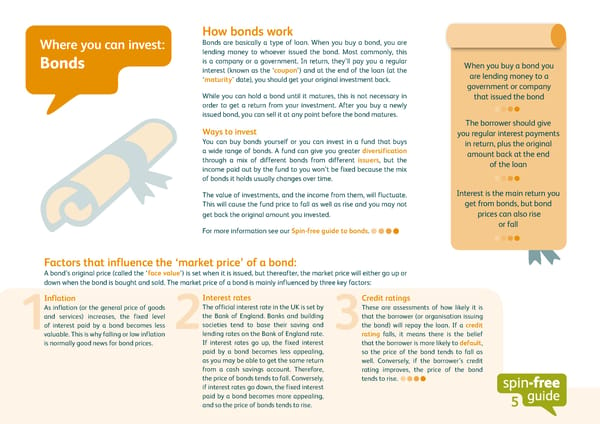

How bonds work Where you can invest: Bonds are basically a type of loan. When you buy a bond, you are lending money to whoever issued the bond. Most commonly, this Bonds is a company or a government. In return, they’ll pay you a regular When you buy a bond you interest (known as the ‘coupon’) and at the end of the loan (at the are lending money to a ‘maturity’ date), you should get your original investment back. government or company While you can hold a bond until it matures, this is not necessary in that issued the bond order to get a return from your investment. After you buy a newly issued bond, you can sell it at any point before the bond matures. The borrower should give Ways to invest you regular interest payments You can buy bonds yourself or you can invest in a fund that buys in return, plus the original a wide range of bonds. A fund can give you greater diversification amount back at the end through a mix of different bonds from different issuers, but the of the loan income paid out by the fund to you won’t be fixed because the mix of bonds it holds usually changes over time. The value of investments, and the income from them, will fluctuate. Interest is the main return you This will cause the fund price to fall as well as rise and you may not get from bonds, but bond get back the original amount you invested. prices can also rise or fall For more information see our Spin-free guide to bonds. Factors that influence the ‘market price’ of a bond: A bond’s original price (called the ‘face value’) is set when it is issued, but thereafter, the market price will either go up or down when the bond is bought and sold. The market price of a bond is mainly influenced by three key factors: Inflation Interest rates Credit ratings As inflation (or the general price of goods The official interest rate in the UK is set by These are assessments of how likely it is and services) increases, the fixed level the Bank of England. Banks and building that the borrower (or organisation issuing of interest paid by a bond becomes less 2societies tend to base their saving and 3the bond) will repay the loan. If a credit 1 valuable. This is why falling or low inflation lending rates on the Bank of England rate. rating falls, it means there is the belief is normally good news for bond prices. If interest rates go up, the fixed interest that the borrower is more likely to default, paid by a bond becomes less appealing, so the price of the bond tends to fall as as you may be able to get the same return well. Conversely, if the borrower’s credit from a cash savings account. Therefore, rating improves, the price of the bond the price of bonds tends to fall. Conversely, tends to rise. if interest rates go down, the fixed interest paid by a bond becomes more appealing, and so the price of bonds tends to rise. 5

How property investing works You can put your Where you can invest: Property investing isn’t just about buy-to-let. Another option is to money in residential invest in commercial property. This means the buildings used by property or commercial Property businesses, such as offices, shopping centres and factories. property What are the advantages? Commercial property offers the potential for a steady return that is mainly made up of the rental income paid by tenants, though there Commercial property is also scope for capital growth. Returns from property investments offers a number tend to be quite different to that from other asset classes, so if you of advantages have a sizeable portfolio, an investment in commercial property for investors over could help you diversify and produce more stable returns. residential property Ways to invest It’s very hard for individuals to invest in commercial property directly, as it tends to require large sums of money to buy a building. Rental Commercial and default – albeit less likely than with residential property – is still a residential property potential disadvantage, along with less liquidity and maintenance offer security of costs. However, this is not all bad news, as there are many funds you income as well as can invest in that either buy commercial property or hold the shares capital growth of companies that manage/develop properties. For more information see our Spin-free guide to property. The differences between residential and commercial property Commercial property is normally a more stable investment than residential property. There are three main reasons for this: Leases The value of investments, and the The leases tend to last much longer – income from them, will fluctuate. five to ten years, compared with the six This will cause the fund price to months to a year of residential letting. 1 fall as well as rise and you may Tenants not get back the original amount The tenants normally have access to you invested. much larger sums of money, so it’s less 2likely they will fail to pay their rent. Notice periods The notice periods are normally longer, so there’s more time to find a new tenant 6 3when a company decides to move on.

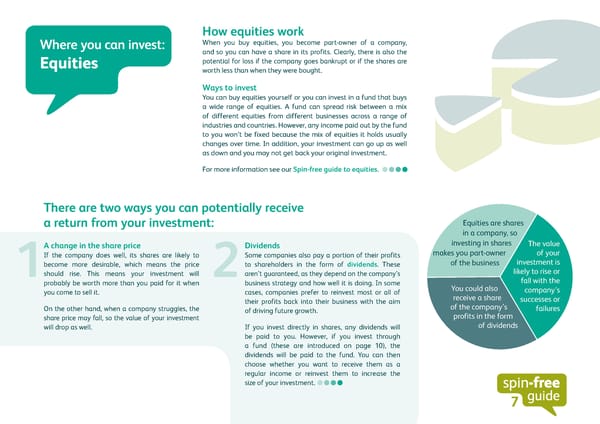

How equities work Where you can invest: When you buy equities, you become part-owner of a company, and so you can have a share in its profits. Clearly, there is also the Equities potential for loss if the company goes bankrupt or if the shares are worth less than when they were bought. Ways to invest You can buy equities yourself or you can invest in a fund that buys a wide range of equities. A fund can spread risk between a mix of different equities from different businesses across a range of industries and countries. However, any income paid out by the fund to you won’t be fixed because the mix of equities it holds usually changes over time. In addition, your investment can go up as well as down and you may not get back your original investment. For more information see our Spin-free guide to equities. There are two ways you can potentially receive a return from your investment: Equities are shares in a company, so A change in the share price Dividends investing in shares The value If the company does well, its shares are likely to Some companies also pay a portion of their profits makes you part-owner of your become more desirable, which means the price to shareholders in the form of dividends. These of the business investment is 1should rise. This means your investment will 2 aren’t guaranteed, as they depend on the company’s likely to rise or probably be worth more than you paid for it when business strategy and how well it is doing. In some fall with the you come to sell it. cases, companies prefer to reinvest most or all of You could also company’s their profits back into their business with the aim receive a share successes or On the other hand, when a company struggles, the of driving future growth. of the company’s failures share price may fall, so the value of your investment profits in the form will drop as well. If you invest directly in shares, any dividends will of dividends be paid to you. However, if you invest through a fund (these are introduced on page 10), the dividends will be paid to the fund. You can then choose whether you want to receive them as a regular income or reinvest them to increase the size of your investment. 7

Managing risk Understanding Wherever you choose to put your money, there will be some level of risk involved. But risk is not necessarily a bad thing. It does mean Risk your investments could fall in value, and you may not get back your original investment, but higher risk also has the potential to produce greater returns. The important thing is to make sure you Risk describes the aren’t taking on any more risk than you need to. potential for losses For more information see our Spin-free guide to risk. Taking some risk is a part of investing There are strategies to help ensure you don’t Here are four strategies to help you manage risk: take more risk than you need to Invest in funds Diversify When you put your money in a fund, it is combined If you hold a blend of investments, they have the with investments from many other people. This potential to perform well, or badly, at different times, 1means it can be spread across a much wider range 2 which reduces the risk of your overall investment of investments than you could buy on your own – so falling significantly in value. One way to diversify you are less exposed to any one holding falling or your investments is to combine higher-risk funds rising in value. focusing on equities with lower-risk funds focusing on property, bonds or even cash. Invest for the long term Invest regularly Markets can drop suddenly at times, often in Investing on a regular basis (such as once a month) reaction to political or economic news. A long-term means you’ll make some investments when markets 3perspective shows that asset price fluctuations 4 are rising and some when they’re falling. This can tend to even out and, over a period of ten years help smooth out some of the ups and downs in the or more, history has shown that markets have markets’ performance. generally risen. 8

A blend of everything Where you can invest: Equities, bonds, cash and property all have advantages and risks. Different funds offer A combination of these asset classes could be an option for some different blends of Multi-asset investors. Investing in different types of assets means you can income and growth create a portfolio with the potential to do what you want, at a level potential of risk you are comfortable with. Find what you need There are many different multi-asset funds in which you can invest. This means you should be able to find one that is balanced for the Holding a blend of asset particular blend of income and growth you are looking for. classes (ie investing in The value of investments, and the income from them, will fluctuate. a multi-asset portfolio) This will cause the fund price to fall as well as rise and you may not can lead to more steady get back the original amount you invested. performance You can do this yourself or invest in a fund that Two ways to create a multi-asset does it for you portfolio You can do this yourself, of course – either by investing directly in a blend of asset classes or by holding a selection of different funds. However, investors can also choose an actively managed multi- asset fund that has the freedom to invest across a range of equities, bonds, property, cash and, at times, currencies. An advantage of this approach is that the investment decisions are made by experienced fund managers, who would look to combine assets that are attractively priced and have the potential to perform differently in different market conditions. Just as importantly, the fund managers should know when to make changes to their holdings in response to changes in the market environment. 9

Some of the ways you can invest In a nutshell You can buy equities and bonds directly – even commercial property You can invest in in some cases – or you can invest in them through funds. These pool many asset classes money from many investors, so they can give you access to a much directly wider range of opportunities than you could invest in on your own. There are then several types of accounts you can hold your funds in. You can hold Alternatively, you your funds in Types of fund Examples of accounts can hold them accounts that available in a fund protect your Unit trusts and Open-Ended Investment investments Companies (OEICs): Individual Savings Account (ISA): from tax You’ll often see unit trusts and OEICs An ISA is not an investment in itself – it’s described as ‘open-ended’. This means they an account that protects your investments can create more units or shares whenever (whether equities, bonds or cash savings) someone wants to invest, so the price of the from tax. In particular, if you are a UK units or shares always reflects the value of taxpayer, you don’t pay capital gains tax on the investment. growth, income tax on interest or higher rate Investment trusts: tax on dividends. These are ‘closed-ended’ funds, which means Junior ISA: they have a limited number of shares. They This has the same tax advantages as an are also companies in their own right, so ISA, but is designed for UK-resident children their shares are traded on stock exchanges. under the age of 18. You can transfer Child As a result, their share price can be higher Trust Funds into Junior ISAs, but you can’t or lower than the value of the investments hold both. they hold. ISA tax advantages depend on your individual circumstances and ISA tax rules may change in the future. 10

Glossary Investment terms The following are explanations of some of the terms you would have come across in this guide. Asset Default Maturity Anything having commercial or exchange value that When a borrower does not maintain interest The length of time until the initial investment Ais owned by a business, institution or individual. payments or repay the amount borrowed when due. amount of a fixed income security is due to be repaid to the holder of the security. Asset class Diversified/Diversification Category of assets, such as cash, equities (or The practice of investing in a variety of assets. This Open-Ended Investment Company (OEIC) company shares), fixed income securities and their is a risk management technique where, in a well- A type of managed fund, whose value is directly sub-categories, as well as tangible assets such as diversified portfolio, any loss from an individual linked to the value of the fund’s underlying real estate. holding should be offset by gains in other holdings, investments. thereby lessening the impact on the overall portfolio. Bond Par value A loan in the form of a security, usually issued by Dividend The initial price of a bond, also known as face value. a government or company, which normally pays a Dividends represent a share in the profits of fixed rate of interest over a given time period, at the a company and are paid out to a company’s Portfolio end of which the initial amount borrowed is repaid. shareholders at set times of the year. A combination of investments held by an investor. Capital growth Equities Risk Occurs when the current value of an investment is Shares of ownership in a company. The chance that an investment’s return will be greater than the initial amount invested. different to what is expected. Risk includes the Face value possibility of losing some or all of the original Coupon The initial price of a bond, also known as par value. investment. The interest paid by the government or company that has raised a loan by selling bonds. Inflation Unit trust The rate of increase in the cost of living. Inflation is A type of managed fund, whose value is directly Credit rating usually quoted as an annual percentage, comparing linked to the value of the fund’s underlying An independent assessment of a borrower’s ability the average price this month with the same month investments. to repay its debts. A high rating indicates that the a year earlier. credit rating agency considers the issuer to be at low risk of default; likewise, a low rating indicates high Issuer risk of default. Standard & Poor’s, Fitch and Moody’s An entity that sells securities, such as fixed income Z are the three most prominent credit rating agencies. securities and company shares. Default means that a company or government is unable to meet interest payments or repay the initial investment amount at the end of a security’s life. 11

Contact us If you would like to get in touch with us you can contact us in the following ways: Call us* Write to us: Customer Relations M&G Customer Relations 0800 390 390 PO Box 9039 If you have a query regarding your M&G investment. Chelmsford CM99 2XG Investment Helpline 0800 389 8600 If you would like to make an investment, request Learning Zone further information on a new or additional investment, Educational guides to help you on your investment or want to read more about our products and services. journey. Our Customer Relations team and Investment Helpline www.mandg.co.uk/learningzone can be contacted from 8.00am to 6.00pm, Monday to Friday, and from 9.00am to 1.00pm on Saturday. Minicom telephone * For security purposes and to improve the quality of our service, we may record and 0800 917 2295 monitor telephone calls. If you have hearing difficulties, you can contact us on If you would like to request a copy of the Important Information for Investors minicom from 9.00am to 5.00pm, Monday to Friday. document, a Key Investor Information Document or the Prospectus, free of charge and in English, please call Customer Relations free on 0800 390 390. This financial promotion is issued by M&G Securities Limited which is authorised and regulated by the Financial Conduct Authority in the UK and provides ISAs and other investment products. The company’s registered office is Laurence Pountney Hill, London EC4R 0HH. Registered in England No. 90776. APR 16 / W124406